The Core 4 Framework is an integrated approach that covers the quality of business, valuations, sentiments and themes, Parag Thakker, Portfolio Manager, ICICI Prudential PMS, says in an interview to Moneycontrol’s Kshitij Anand. Edited excerpts:

Q) ICICI Prudential PMS Large-cap Strategy, a diversified theme, outperformed other PMSes in May, data from PMSBazaar.com shows. What is the core strategy of the theme that helps you pick winners?

A) Our stock selection process across all our PMS strategies is guided by a Core-4 investment framework. The Core 4 Framework is an integrated approach that covers the quality of business, valuations, sentiments and themes.

This core investment philosophy has not only helped to ride through turbulent markets in the past but it has also helped to negotiate the recent market volatility.

Q) Can you elaborate on the investment framework?

A) In the first part of the investment framework, we aim to focus on companies with established business models, having low leverage and which are believed to be able to generate sustainable cash flows.

An internal study of past market cycles has shown that companies with lower debt have been able to negotiate a crisis better and, in some cases, have been able to recover faster.

In line with our framework, valuations are equally important because if one does not buy it at the right price, the entire analysis will likely to be futile. Market events, both domestic and global, can easily spark a change in sentiments.

Thus, one of the best times to invest is when the sentiments are considered to be unfavourable or seem to be at a turning point. Further, portfolios being overweight on dominant themes have the potential to capture a market upside.

In the various phases of a market cycle, investment themes can either be dormant or dominant. Alpha is likely to be created by riding dominant themes.

The current market environment has been conducive for all the above factors, which is why ICICI Prudential PMS Large-cap Strategy for the month of May 2020 returned 3.62 percent, compared with -2.55 percent of the benchmark S&P BSE 100.

This translates into an alpha of over 5 percent. Not only in the one-month period, across the one-year, three-year and five-year periods, this strategy has been able to outperform the benchmark (refer the table below).

Aggregate Performance of ICICI Prudential PMS Largecap Strategy (Strategy)

(Returns less than 1-year are absolute, greater than 1 year are on annualized basis. Past performance may or may not be sustained in the future. The Strategy performance mentioned above is the aggregate performance of all clients in the Strategy using the time weighted rate of return (TWRR) methodology and the performance of an individual client may vary significantly from the above.)

Q) Markets have turned volatile following the coronavirus outbreak and growth has slowed down across the world. Did you tweak your portfolio strategy to minimise the impact of volatility?

A) One of the primary reasons for alpha generation in the past few months is that the portfolio has been extremely underweight to banks and finance.

We had begun reducing exposure to financials since the beginning of November 2019, as the sector seemed to look overvalued. This has helped limit the downside considerably when the market corrected.

The portfolio has been overweight on pharma, this helped capture an upside that we have seen in pharma stocks. Post the sharp rally, we have reduced our exposure to the pharma sector.

We were also overweight on telecom and gradually increased exposure to select consumer names, which have helped the portfolio in the past few months.

Active sector rotation has helped the Strategy not only to limit a downside but to capture an upside as well.

Q) The Strategy, which started off in March 2009, has given a stable performance of more than 8 percent in CAGR terms. What were your key learnings from the last decade and how can we relate to the current environment?

A) One of our key learning’s has been to invest in companies where you understand the business and its track record of efficient capital allocation. This can be derived from their business dealings.

In addition, businesses having low leverage, low CAPEX requirement and low working-capital leakage are generally preferred. This, in turn, may lead to good operating cash flows and the least possible interest cost.

Businesses having a sizable market share in their respective sectors are also an important factor.

Based on our experience, we believe that the best time to buy such companies is during a bad phase of the market or due to a big negative external event or forced non-fundamental selling. This is what we believe could be a recipe for generating better returns.

Q) Largecap stocks have become slightly more expensive because money is now chasing only those companies that have a strong balance sheet and robust growth prospects, especially at a time when growth has taken a hit amid COVID-19 outbreak. What are your views?

A) Certainly, money is likely to flow to the companies that exhibit the potential to ride out the current crisis. While having a healthy balance sheet and growth prospects is important, it is equally important to focus on companies that are able to generate sustainable cash flow and at the same time have low debt on their balance sheets. No one knows how this pandemic will pan out.

Thus, the priority shifts towards companies that are in a position to survive in case of a prolonged economic slowdown. We prefer companies with a proven business model, run by effective management having a strong competitive edge and which have been able to maintain a sustainable market share.

Even in our ICICI Prudential PMS Contra Strategy, we are now focusing on large companies, where valuations seem to be reasonable, which are likely to generate cash flows and which are believed to be least impacted by the lockdown.

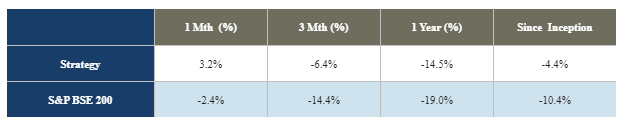

In the past month, this Strategy, too, has managed return 3.24% vs a negative 2.42% over the S&P BSE 200 benchmark.

Q) What differentiates the Contra Strategy?

A) ICICI Prudential PMS Contra Strategy is a diversified Strategy that has the flexibility to invest across market caps and is sector agnostic. We aim to invest in companies that are currently not in favour in the market but are expected to do well in the long run.

We also aim to invest in sectors where entry barriers are high, sectors that are in consolidation or companies in special situations.

The Contra Strategy was launched on September 14, 2018, and has outperformed the benchmark with an alpha of about 6 percentage points since its inception period as on May 31, 2020 (refer the table below for performance).

Aggregate Performance of ICICI Prudential PMS Contra Strategy (Strategy)

This was at a time when domestic cyclicals were facing issues mainly due to tight liquidity, high crude, falling rupee, rising concerns on fiscal deficit, these private sector banks stood out with a good liability franchisee and potentially robust capital structure.

Given the issues faced by the NBFC sector and PSU banks, the exposure to private sector banks seemed to have worked well for the Strategy and contributed to the returns.

In August 2019, negative news flows around the consumption sector had led to attractive valuations. This is when we took exposure to a biscuit manufacturer, that too, helped to contribute to returns.

Similarly, the strategy took exposure in a few insurance companies when they had corrected due to non-fundamental reasons. These are some examples of our contrarian calls that helped the Strategy to generate alpha.

Q) How do you see the India-China standoff impacting markets in the near term? Do you think if tensions escalate the Nifty can go towards 7,500 despite positive global cues or liquidity?

A) It is difficult to predict how the markets will react to a geopolitical event. The ongoing pandemic has already created a lot of uncertainty. It is impossible to predict if easy money will continue to drive the market or whether India-China tensions will lead to a correction.

However, we do believe that the healthy fundamentals of the companies held in our portfolios may help them to emerge less impacted by such a crisis.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!